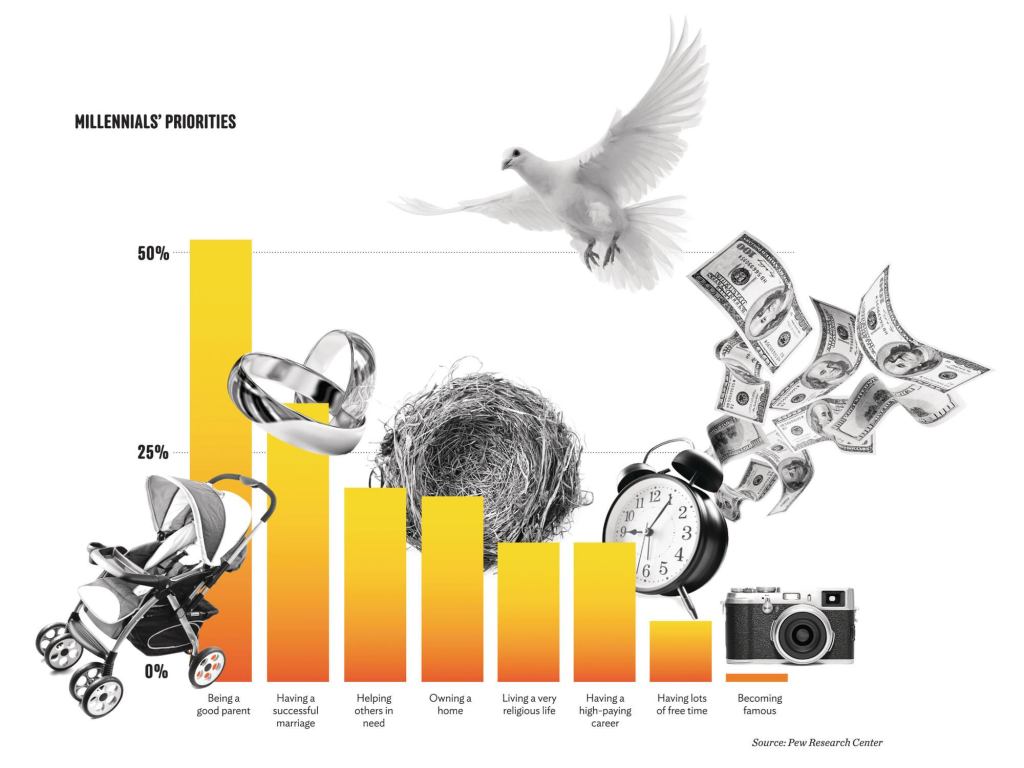

Survey Says: Millennials Want Instant Gratification

By 2014, Millennials will make up 36 percent of the country’s workforce. Currently, the demographic is on pace to reach 80 million this year.

The Boston Consulting Group (BCG), along with Barkley and Service Management Group, recently surveyed 4,000 Millennials to try to understand what makes them tick when it comes to their consumer behaviors. And the success or failure of many types of businesses will hinge on the degree to which they can cater to this voluminous generation.

“Millennials already shell out and influence the expenditure of hundreds of billions of dollars annually—an amount that will only increase as they mature into their peak earning and spending years,” the survey reports.

The survey also found that the generation is obsessed with instant gratification. In fact, they shop for groceries at convenience stores twice as often as non-Millennials. For apartment firms, this means that customer-service models need to reflect the speed, ease, and efficiency the group has come to demand.

And this is a generation actively engaged in consuming, and influencing. Millennials are far more engaged in online activities, like rating products and services, than non-Millennials (60 percent versus 46 percent). And about 60 percent of them regularly upload videos, images, and blog entries to the Web, versus 29 percent of non-Millennials. The report shows that this focus on technology is a key determining factor in how they spend their money.

“Millennials also tend to seek multiple sources of information, especially from noncorporate channels, and they’re likely to consult their friends before making purchase decisions. More Millennials than non-Millennials reported using a mobile device to read user reviews and to research products while shopping (50 percent versus 21 percent),” the report says.

The recession hit Gen Y especially hard. Now, this demographic faces some tough economic choices, especially when it comes to housing. And that’s a subject Nicole Lapin, a former CNN and CNBC anchor, knows something about.

Lapin is now the CEO of New York City–based Nothing But Gold Productions, a multimedia company that creates accessible financial content across multiple platforms. In her role, she’s seen firsthand some of the financial challenges Gen Y is facing. She recently shared her thoughts on the subject with Multifamily Executive and discussed the age-old question: Is it better to rent or own?

MFE: What are some of the biggest financial challenges Gen Yers face today?

Lapin: The numbers are scary. The number of young people looking for jobs is higher than ever: The unemployment rate for young people is currently upward of 20 percent. Student debt now totals up to $550 billion—a significant part of the nation’s debt. College costs have risen 1,000 percent in the past 30 years, outpacing health care, which has risen 700 percent, and inflation, which has risen “only” 300 percent. Minimum wage in the last 10 years has increased negligibly compared with the increase of student debt, which has risen a whopping 511 percent just since 1999. We’re creating a true “lost generation” of overeducated, overleveraged, underpaid young people, and I truly believe that this is the next major fiscal bubble to burst.

MFE: How are finances influencing where Gen Y lives (in terms of their housing options)?

Lapin: As much as pop culture jokes about “moving back in with the ’rents,” it’s become a reality for many young American women and men—especially the latter. While the share of women living with their parents has remained a fairly steady 10 percent since 2007, the share of men living at home has increased from 14 percent to nearly 19 percent in the same amount of time.

A recent report found that more than one-third of young people rely on their parents for financial support. Even for those who are gainfully employed, 69 percent say they don’t make enough money to live the lifestyle they aspire to. So for those not living at home, we’re seeing a lot of cramped living situations, or long commutes to and from work—which, let’s remember, means even more money spent at the pump!

MFE: Are micro units the answer? Should cash-strapped Millennials consider moving to smaller living spaces in core markets?

Lapin: Again, it’s all about location here. If you get a place that’s cheaper but really far away from the nearest subway or work, you could wind up spending more in commuting costs. Remember that “newer” doesn’t automatically mean “more expensive”: Many newer units feature energy-efficient appliances and in-apartment laundry units, both of which can save you on utility bills in the long run. Pay attention to the smaller details: If the apartment is on a lower floor, or in back of the building, chances are the rent will be lower, too. And use your best negotiating skills: In this market, anything goes!

MFE: For recent graduates entering the housing market for the first time, is it better to rent or buy?

Lapin: It used to be that putting a down payment on a house or apartment was the surefire way to boost your net worth, but in this market, it can be more beneficial to look at renting. Buying a house comes with tons of additional costs—transaction fees for the broker, maintenance fees, renovations—while many of those costs are included when you rent an apartment. Remember that down payment is typically about 20 percent of the mortgage. You don’t get that money back like you do a security deposit. And today’s Gen Y is so mobile: Renting allows you greater flexibility to take any troubles (or opportunities) that might come your way.