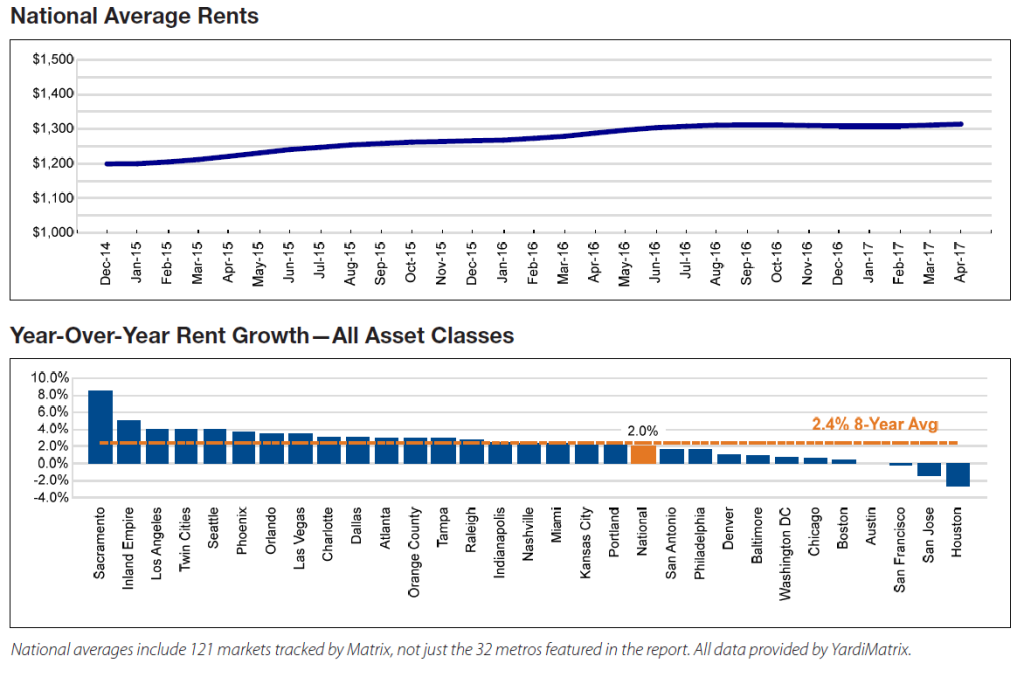

The average U.S. multifamily rent rose by $3 in April, reaching $1,314, according to Yardi Matrix’s monthly survey of apartment markets. At the same time, the national rent-growth rate has slowed to below long-term growth trends. Rents rose by 2.0% in April on a year-over-year (YOY) basis, down 50 basis points (bps) from March. This represents a significant drop from the 5.5% rent growth seen a year ago.

The Matrix Monthly report has long anticipated this deceleration, given the rapid increase in new apartment supply and the unsustainable rent growth in some metros. The current rate of growth is more in line with historical growth rates, however, and with current wage growth, according to Yardi. At the moment, rents have peaked above the level of affordability for the average resident.

New-unit delivery is at a cyclical high, with over 363,000 units expected to come on line this year. Roughly 80% of these units serve the “Lifestyle” renter segment, defined by Yardi Matrix as properties aimed at high-income households that choose to rent despite having enough wealth to own. Much of the unit demand rests in the “Renter by Necessity” (RBN) segment, with middle-income renters who demand market-rate properties. Nationally, RBN property rents have increased by 3.3% YOY, while Lifestyle property rents have increased by 0.7%. New supply is expected to decline in 2018–2019.

Occupancy of stabilized properties grew to 94.8% nationally in March, 10 bps above February’s rate. (Matrix Monthly occupancy data are presented from the month previous to that of rents and rent growth.)

The impact of these trends hits hardest in metros with heavy supply growth and high rents. The Houston market sports the biggest difference between RBN rent growth (0.5%) and Lifestyle rent growth (-4.7%) YOY.

Trailing Three-Month and 12-Month Rent Growth

On a trailing three-month (T-3) basis, a measure of short-term changes in rent growth, apartment rents increased by 0.1% in April, matching the pace set in March. Lifestyle rents remained unchanged, while RBN rents grew by 0.2%. On a local level, Lifestyle rents remained flat or fell in half of Matrix Monthly’s top 30 markets, whereas RBN rents grew in 24 of the 30 markets.

Sacramento, Calif., led all markets in overall T-3 rent growth, at 0.6%. Houston and Austin, Texas, are both declining on this scale, at -0.3%. The Twin Cities and Seattle sport the strongest Lifestyle rent growth, at 0.5% each, while Charlotte, N.C., has the strongest RBN rent growth on a T-3 basis, at 0.6%.

On a trailing 12-month (T-12) basis, rents grew by 3.8% in April, down 20 bps from March. RBN rents grew by 4.8%, a rate that now exceeds Lifestyle rent growth by 200 bps. Yardi notes that a high supply of new upscale units has limited the pricing power of many apartment owners in large markets.

Sacramento leads overall T-12 rent growth, at 9.9%. Yardi notes that the Sacramento market is relatively more affordable than the Bay Area but that it still has strong job growth and limited supply.

Looking Ahead

Yardi Matrix anticipates “rocky” rent growth over the next 12 to 24 months as the market reacts to the coming wave of new apartment supply. San Francisco, Denver, and Austin, which all experienced double-digit rent growth as recently as 18 months ago, are now experiencing flattening or declining rent growth as new supply comes on line. Yardi Matrix anticipates that deceleration will also soon reach markets like Charlotte, where new completions make up 5.8% of total stock, as well as Nashville, Tenn., (4.9% of total stock) and Miami (3.5% of total stock).

The report reiterates Yardi’s previous outlook on the overall health of the market and strong fundamentals. Job growth is robust, although slow wage growth will limit rent growth. Above-trend growth may not reappear for a few more years, but Yardi predicts that 2017 will be the “high-water mark” for apartment completions, and that the market has “significant long-term upside potential.”