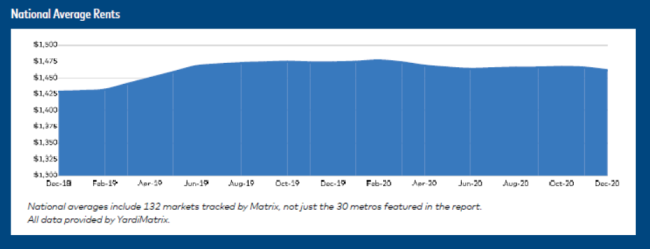

The national average multifamily rent fell by $4 to $1,462 in December, marking the steepest one-month decline since the start of the pandemic, according to Yardi Matrix’s latest Multifamily National Report. Overall, multifamily rents fell by 0.8% YOY in December, marking a 30-basis point decline from November’s rent growth.

According to Yardi Matrix, “2020 will go down as the year COVID-19 changed everything.” Despite initial fears that the pandemic would depress rents across the country, in the end many metros have ended 2020 unscathed or with significant rent growth. At the same time, expensive coastal markets have seen significant declines, reflecting the ongoing “extreme bifurcation” in market growth and performance.

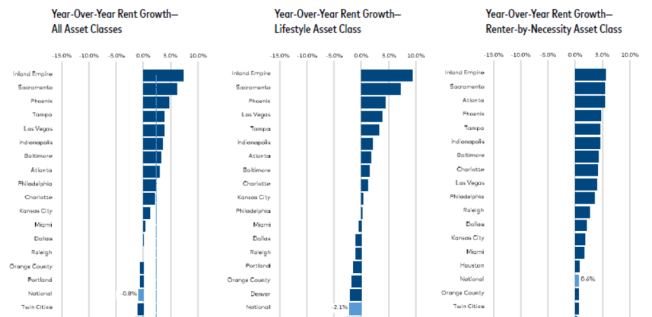

California’s Inland Empire tops the list for rent growth YOY at 7.3%, followed by Sacramento at 6.1%. These markets have held the top two positions for the last four months. At the bottom are San Jose at -13.7%, followed by New York at -11.7%. San Jose has been at the bottom of the top 30 markets for seven consecutive months, and the metro’s overall rent has fallen by 14.1% since March.

Yardi attributes this stark difference in rent growth patterns to a mass exodus from gateway markets and ongoing growth in lower-cost, lower-density areas. Job losses and remote work are ongoing factors in this shift, as well as the high costs of living in gateway cities and the closure of urban amenities. For instance, stark rent declines in New York and San Francisco parallel strong rent growth in Long Island and White Plains, New York, as well as Sacramento and the Inland Empire.

Rents declined by 0.3% on a month-to-month basis in December, marking a 20-basis point decline from November’s month-to-month rent growth. Tampa led the top 30 markets in rent growth at 0.9%, followed by the Inland Empire, Orange County, and Phoenix at 0.5%. Eighteen of the top 30 markets experienced a short-term rent decline, with 19 out of 30 seeing declines in luxury “Lifestyle” rents and 17 out of 30 seeing negative market-rate “Renter by Necessity” growth. San Jose saw the largest month-over-month decline at -2.4%, followed by Seattle at -1.3% and San Francisco at -1.1%. Austin rebounded to 0.4%, up from the bottom five markets in November to the top five markets in December.

According to the NMHC’s Rent Payment Tracker, 93.8% of professionally managed apartment rents were fully or partially paid by the end of December. Yardi expects rent collections to hold up in the near future, given the passage of the pandemic relief bill and the potential for additional stimulus in the coming months. In addition, by the second half of 2021, Yardi anticipates that the vaccine distribution process across the U.S. will be “coming to an end,” at which time a full economic recovery can begin in earnest.