The affordable housing finance industry posted another strong year in 2011.Low-income housing tax credit (LIHTC) prices rebounded in a big way, climbing up in a year when both LIBOR and the 10-year Treasury dropped to historic lows.

Another trend that characterized 2011 was the idea among a growing number of private and public lenders that affordable housing could be a highly profitable enterprise.

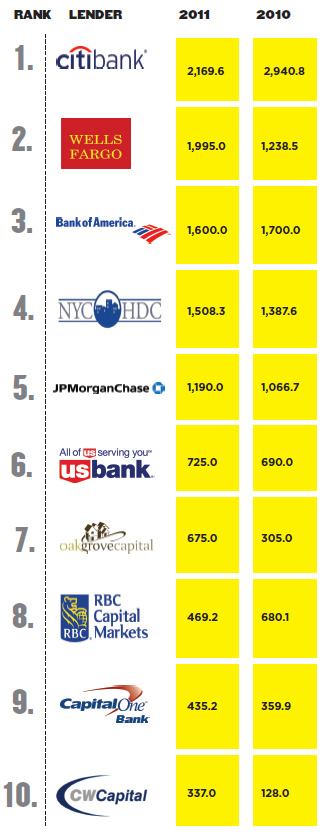

Oak Grove Capital more than doubled its production last year, climbing up five spaces to break into the Top 10 for the first time in our sixth annual survey. But the “most improved” award goes to fellow agency lender CWCapital, which catapulted 15 slots, reaching 10th on this year’s list. Last year, the lender started an affordable housing debt platform and launched a LIHTC syndication business, hiring Andrew Weil and Justin Ginsberg away from Centerline Capital Group to run the program.

And it’s not just agency lenders—many large banks, whose affordable housing strategy was driven solely by compliance in the past, are now stepping outside of their Community Reinvestment Act (CRA) footprints to reap greater profits.

“Meeting and exceeding our CRA goals will always be important,” says Kyle Hansen, executive vice president at Minneapolis-based U.S. Bank. “But we’re a healthy institution that’s very interested in increasing our lending activities broadly, and if we can do that profitably out of footprint, then we’re going to actively do that.”

Like U.S. Bank, JPMorgan Chase also hopes to increase its community development lending operations this year—not because it has to, but because it wants to. The bank grew its affordable housing volume by more than 11 percent last year and hopes to grow another 15 percent this year.

“The business has proven out to be successful, and one that has opportunity to grow. But to grow the business, we need to move outside of our footprint states,” says Ed Sigler, head of community development real estate at New York–based JPMorgan Chase Bank. “There are places like Boston, Minneapolis, and Nashville where we’re not currently active, because they’re not part of our footprint, but we think they’re good markets and there are good deals there.”