Even among private, regional companies, the M.O. for 2010 is stack and attack, and the industry seems poised to deploy capital as soon as there is a semblance of normalcy to the transaction market and a bottoming out of rent fundamentals. “We just closed a fund of $200 million in equity that is liquid and available to us to acquire and develop multifamily real estate,” says Western National president Thomas Shelton. “There have just been a few transactions, and value is still bouncing around the board. We have expectations on the returns that we need to make, and as soon as we see the prospect of those returns, we will invest accordingly.”

7. Expect Cap Rate Compression.

With gun-to-the-head mentality among sellers still a somewhat rare market event, bid/ask spreads remain preventively wide in terms of fostering a healthy transactional environment for multifamily apartment stock. The oft-mentioned disconnect between buyers and sellers as a hindrance to deal flow is expected to close in 2010, and it’s not just sellers that will be moving the gap. Multifamily properties currently on the block are fetching 20 or 30 bids per go, and that kind of interest—coupled with an uptick in volume—is the perfect recipe for cap rate compression.

“You are starting to see evidence of buyer appetite for good quality, relatively low-risk properties on the market at more reasonable prices,” says Marcus & Millichap managing director of research Hessam Nadji. “On good quality assets in primary markets, we are receiving 20 offers with cap rates compressing 30 to 50 basis points based on buyer competition alone.”

Absent hikes in interest rates and the deployment of capital in the acquisitions and disposition market could even push cap rates down to pre-recessionary levels. “When things start getting better, you’ll find that there are a lot of people out there willing to buy assets at cap rates not different from what we have seen in the past,” says ZOM’s Patterson. “I don’t subscribe to the belief that we are going to see cap rates rise 100 basis points: We already see quality deals selling now at 6 percent cap rates.”

8. Locate Lending.

Executing on acquisition deals, regardless of cap rates, will still necessitate debt financing for many. That financing is still likely to come from Fannie Mae, Freddie Mac, or FHA multifamily lending programs, and even those dependent on agency debt are looking at stricter underwriting requirements and more stringent loan terms. Likewise, banks re-entering the multifamily debt markets—whether for acquisition or even new development—have reset the bar on underwriting and leverage expectations.

Mike Peter, CEO of Austin, Texas-based Campus Advantage, echoes an industry chorus when he says it’s time for multifamily players to simply expect those lending realities. “Leverage ratios are changed, and the guarantees that lenders are requiring on projects are much more onerous and a little bit shocking for many,” Peter says. “But we develop in Canada as well and a lot of these underwriting requirements have been standard outside of the U.S., and those markets have fared much better because of it.”

On the construction side, debt is more of a critical issue with banks still largely unwilling to extend capital into the development space. Still, some players have found success—albeit with higher equity and underwriting requirements—working with regional banks that were not over-extended on real estate. “The lenders are out there but they are cautious,” says Pittro of RMK, which just broke ground on a downtown apartment complex and is looking to commence development on two other projects in 2010. “If you are a good company with a good relationship, you will find funding. And by relationship I mean a lender you have been working with for 20-plus years.”

CAPITAL AND COSTS

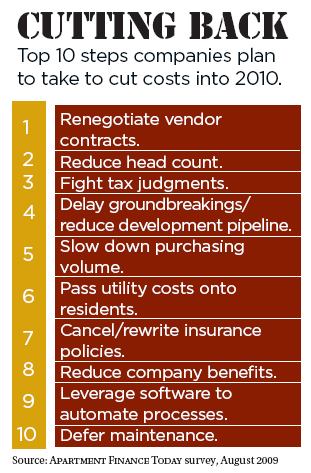

9. Trim Excess—and Yes, There is Some.

In late 2008, Connor challenged his firm from top down and bottom up to do three things: identify ancillary revenue opportunities; continue to improve the company’s twice-yearly Gallup survey customer service scores; and find $5 million in excess costs to cut from The Connor Group’s books.

The firm delivered, finding savings in operational costs, purchasing, and in the renegotiation of vendor contracts to ultimately best their challenge by $600,000. Even in organizations already stressed from squeezing blood from the stone, creative thinking can typically find additional cost savings. “Look at your hours, for instance,” advises RMK’s Pittro. “Do you really need to be open six hours on Sunday? Maybe you can do that in five. Those are the types of savings, too, where your team will be very appreciative of anything you can do as opposed to laying off people.”

Don’t forget about spending a little money to make some money. Campus Advantage used 2009 to purchase and install biometric time clocks at most of its locations for better payroll efficiency. “The clocks have enabled us to be much more accurate with labor hours and avoid unnecessary costs to the property,” says CEO Peter of the palm-scanning devices. “The clocks paid for themselves in a couple of months, and there’s only one trick to override it.”

10. Rework Tax Assessments.

Cost-conscious multifamily operators could also do well to continue wearing down assessors when it comes to property insurance and real estate taxes. Especially given the near national depreciation in both property values and NOI, 2010 will be a critical year for taking it to the Tax Man before a broader economic recovery initiates asset value rebounds.

“There’s no question that values are down across the country,” says Western National’s Shelton. “We are going back to assessors and asking for reductions in taxes and reductions in valuations. Obviously, the municipalities rely on those taxes to pay for their operating expenses, and they are quick to use sales comps and cap rates from before the market turned. It’s a challenging exercise, but you can have success in getting them to at least meet you half way.”