Given the shift to working from home, whether by preference or by necessity, RENTCafe researcher Sanziana Bona notes that the suburbs have a “newfound appeal” for renters, as they often offer larger apartments, lower density, and lower rents than big cities. Based on Yardi Matrix data for large-scale apartment buildings of 50 units or more, the markets best equipped to meet this new demand are those where the multifamily supply has already been expanding, with a spike in population growth—and in turn new apartment construction—over the past five years.

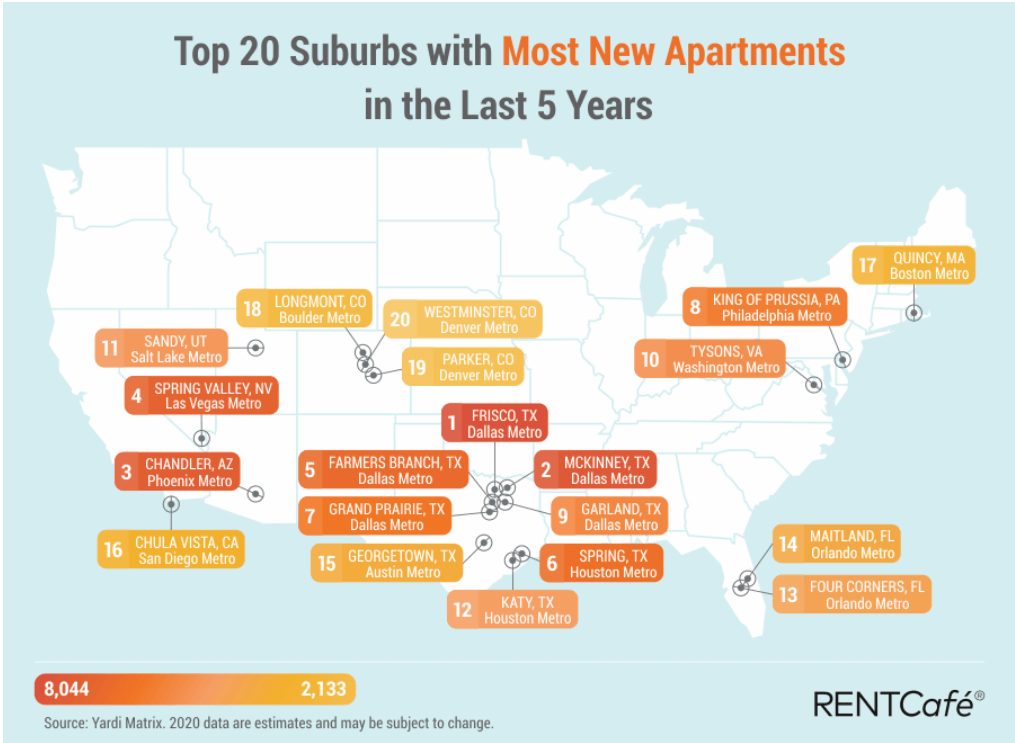

Frisco, Texas, is first on the list with 8,044 new apartment units in the last five years—almost double the next city. New construction makes up 42% of the city’s apartment stock, across 25 new large-scale apartment properties. McKinney, Texas, also in the Dallas metro, comes in second with 4,843 apartments across 10 new large-scale buildings in the last five years, or 30% of the city’s apartment stock.

Altogether, Texas markets make up six of the top 10 on this list, and eight of the top 20. Colorado comes in second, with three suburban markets in the top 20, followed by Florida, Arizona, and Nevada. Twelve out of the top 20 are located within 20 miles of an urban center.

Out of the top 20 markets, Maitland, Florida, ranked No. 14, has the highest share of new apartment units as a percentage of total stock at 77%. This accounts for 2,283 new apartment units in the past five years across eight buildings. King of Prussia, Pennsylvania—No. 8 and one of only two Northeast markets in the top 20—has also built more than half of its new apartment stock in the past five years, with 3,030 new units across nine buildings accounting for 51% of large-scale apartments. No. 16 Chula Vista, California, has the lowest share at 12%, with 2,174 units across seven new properties.

Click here to view the full list.