Courtesy UDR

Inwood West, a 446-unit property in Woburn, Mass., was acquired …

With apartment transaction volume still stuck in neutral last year, the management team at Arlington, Va.–based REIT AvalonBay Communities (AVB) needed to find a creative way to meet their stated goal of adding more Class B properties to their portfolio.

So, much like the general manager of a baseball team, they started to look at trades. “In the middle of last year, we did a deep dive on [our competitors’] portfolios across our markets that match what we’re trying to achieve,” says Tim Naughton, COO at AvalonBay. “We contacted a number of public and private companies.”

Fellow REIT Denver-based UDR seemed like a good fit. The company had Class B assets in Southern California. “[AvalonBay] was looking to expand its portfolio in Southern California,” says Tom Toomey, CEO of UDR. “We both agreed it was a competitive market to buy and sell in.”

In April, the trade went down and both companies seem to have achieved what they wanted—AvalonBay increased its Class B holdings by 1,418 units; UDR acquired 1,060 units, helping it grow to 59,749 units overall. And analysts who are paid to monitor the companies think it might have a result that’s fairly rare given today’s propensity to pick instant winners—this deal looks to be a win/win for both sides.

Complementary Goals

Since the mid-2000s, AvalonBay has been working to reshape its portfolio. “The objective is to buy assets best positioned in target submarkets where we want to play,” Naughton says. “In some markets, it’s [Class] B product; in other markets, it’s Class A product. It’s more about drilling into the submarkets where we want to do business and trying to understand which assets will outperform based on NOI.”

By virtue of that strategy, AvalonBay would like to add a bigger percentage of Class B assets to its portfolio. Rather than having 85 percent As in its portfolio, it wanted to slide that ratio down to about 75 percent. “If we compete in 200 to 300 submarkets, a little less than half the time, the As outperform,” Naughton says. “But about half the time (or sometimes a little more) Bs have outperformed.”

Meanwhile, last November, UDR announced it had bought Houston-based Hanover Co.’s interests, which included 5,748 units and one land parcel, in a partnership between Hanover and MetLife. In all, it has changed its portfolio by 20 percent in the past eight months and has shown a capacity to take on complicated deals. “It helped us accomplish what we’re trying to achieve, which was to grow in Boston and San Francisco,” Toomey says. “It made it easy that both of us had objectives, and we also had surplus assets in the markets that we were both looking to expand into.”

Naughton agrees: “They wanted to get more penetration in Boston and San Francisco—we have a deep development pipeline engine in Boston. And we wanted more penetration in Southern California—we wanted more moderately priced units in supply-constrained submarkets and UDR had a big presence in those.”

The Negotiation

With approximately 36 assets (comprising 9,513 units) in Southern California, UDR definitely had the portfolio to entice AvalonBay. But there was still some “horse-trading,” as Naughton calls it, to lock down the specific assets that would change hands.

“We just negotiated which assets made sense,” Naughton says. “It wasn’t just from portfolio allocation objectives, but also things like debt that may have been on them or certain constraints, whether it’s performance or encumbrances.”

To make the trade, the companies first had to agree on overall market values. “It’s important to have that discussion before you start to talk about the individual assets,” Naughton says. “You have to talk about what cap rates in the market are and what the cap rates are for these quality assets versus different quality assets. If you don’t have that, it will be difficult to pull [the trade] off.”

The REIT Way

Here are three reasons why it’s easier for REITs to pull off an exchange of assets.

1. Ownership clarity. Many REITs own their assets outright. Privates often have different investors who will want to sell for the highest possible value instead of doing an exchange.

2. More assets to use. “Publics have more pieces on the table,” says Tom Toomey, UDR’s CEO. “That gives them more options and flexibility. Privates don’t have as many pieces on the table.”

3. Similar objectives. “REITs tend to be more strategic about portfolio allocations than the private guys,” says Tim Naughton, COO at AvalonBay Communities. “Privates tend to be more opportunistic. They’ll be looking to get the better of the trade as opposed to it being a win/win.”

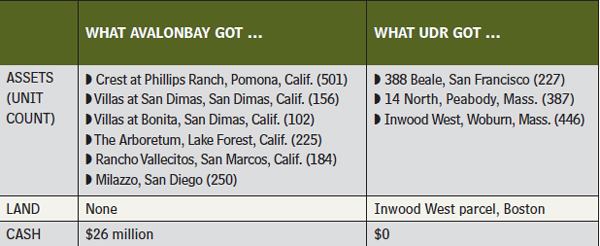

The companies then batted around assets, reviewing several properties. Eventually, AvalonBay agreed to trade three apartment communities (two in Boston and one in San Francisco) and a small land parcel in Boston for six UDR apartment communities (all in Southern California) and $26 million in cash.

“It’s baseball,” Toomey says. “You say, ‘Here is all of my farm system, and here are all of the players.’ You kind of look to structure a deal that basically fits [each side]. There were assets that we rejected and assets they rejected out of the trade. Ultimately, it just got into right-sizing, and that’s how it works in a trade.”

Naughton says AvalonBay sees value in all of its purchases, but Milazzo in San Diego and Rancho Vallecitos in San Marcos, Calif., offer strategic significance. “We’re trying to build a presence in San Diego,” he says. “We’re glad to get a couple of assets there. We weren’t at a critical mass in San Diego. This helps us get closer.”

For UDR, the deal offers great benefits as well. “I like the suburban Boston stuff,” Toomey says. “It’s quality-built and quality-located, and it will do well over time. It’s also hard to find San Francisco high-rise towers [like 388 Beale]. It is well-constructed and well-located.”

A Win/Win

Being public companies, both UDR and AVB face a gauntlet of analysts every quarter. When they undertake a larger deal, like their trade in April, they’re going to get reaction. In this case, it was fairly positive, with many analysts referring to the transaction as a “win/win” for both sides.

“In the AvalonBay/UDR deal, both companies achieved their goals. It was a win/win,” says Alexander Goldfarb, managing director of equity research of REITs for New York City–based Sandler O’Neill + Partners. “It was a good transaction. UDR wants to reduce its holdings in Southern California and bulk up in Boston, while AvalonBay wants to reduce exposure to Boston and bulk up in Southern California and B assets.”

Goldfarb also likes the deal because the companies avoided brokerage fees by using their own folks to do the underwriting and its efficiency. “Effectively, there was no cash,” he says. “Neither firm had to raise equity or debt.”

Other analysts agree. “It made strategic sense for both parties,” says Andrew J. McCulloch, an analyst for Newport Beach, Calif.–based Green Street Advisors.

While Naughton doesn’t expect to make another trade like the one the company made with UDR, he won’t close the door on it. In fact, since the deal was announced, AvalonBay has fielded calls from others interested in trades. “A number of people have seen it, and it has gotten them thinking about it,” Naughton says. “We have had a couple of superficial discussions with some guys who are just batting around some ideas.” [M]

Insider Trading

At right is a breakdown of the dealing and wheeling that got REITs AvalonBay Communities and UDR exactly what each wanted.