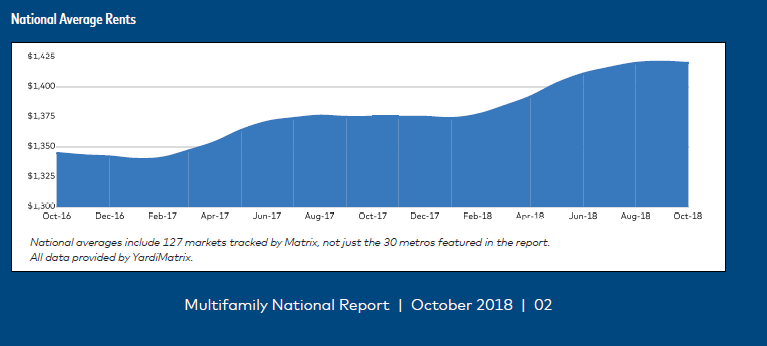

U.S. multifamily rent growth lay flat for the second straight month in October, falling by $1, to $1,420, while year-over-year (YOY) rent growth was unchanged from September, at 3.3%, according to Yardi Matrix’s Matrix Monthly report for October 2018.

The YOY rent-growth level has increased by more than 100 basis points (bps) in the past 12 months. Market-rate rent growth has far outpaced rent growth in luxury properties, 3.9% to 2.6%, a gap of 130 bps.

While flat prices and moderate growth point to a seasonal slowdown at the national level, Yardi notes that rent performance varies widely by metro, with the strongest gains in the Southwest. Las Vegas, for example, experienced its healthiest rent growth since the beginning of the year, at 7.4% YOY through October, up from 5.8% in January. Phoenix experienced a similar meteoric rise, up to 7.0% YOY through October from 4.0% in January.

Yardi attributes these markets’ growth to low new supply and high demand, along with high employment growth and in-migration in Phoenix. Only a few of the nation’s top metros have rent-growth rates below 2%, with Houston the lowest, at 1.6%.

T-3 Rent Growth

Rent growth fell to 0.1% in October, down 10 bps from September and 50 bps from July, on a trailing three-month (T-3) basis, which compares growth from the past three months with growth in the previous three months.

Las Vegas also led the nation in rent growth on a T-3 basis, at 0.8%, followed by Phoenix, at 0.6%. Boston, Seattle, and San Jose, Calif., all experienced -0.4% rent declines over this period. Some metros have experienced rent-growth drops concentrated in the high-end segment on a T-3 basis, including Boston (-0.7%), San Jose (-0.6%), and Chicago (-0.5%). Yardi attributes these losses to a rising supply of new luxury units.

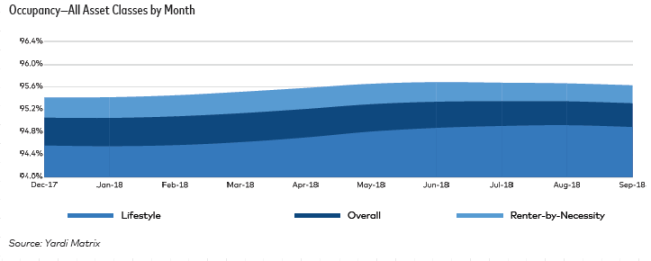

Despite ongoing supply growth, occupancy rates have remained stable at their present high levels.

Multifamily Housing and the Midterm Election

When the Republican-run House flips to Democrat control in January, Democrats will gain the power to write the federal budget and to act as a check on the Trump administration. A divided Congress may reduce the likelihood of significant legislation being passed, according to Yardi, though the current Congress may rush to pen bills before the end of 2018.

Several state governorships have also changed parties, which may affect housing policy at the state level. New Mexico, Nevada, Kansas, Wisconsin, Illinois, and Maine have flipped Democrat, while Alaska has flipped Republican.

Both the partisan and policy divide between Republicans and Democrats make legislative government-sponsored enterprise (GSE) reform and further bank-regulation rollbacks unlikely after January. Yardi notes that Jeb Hensarling, current chairman of the House Finance Committee, has tried for some time to dismantle the GSEs, while his counterpart in the Senate, Mike Crapo, has approached the issue from a bipartisan standpoint. The incoming chairwoman of the House Finance Committee, Rep. Maxine Waters (D-Calif.), is expected to focus on housing affordability.

Since Trump will soon get to appoint a new head of the Federal Housing Finance Agency, conservator of the two GSEs, his appointee may have more power to affect Fannie Mae and Freddie Mac than the legislative branch will. There are limits to the changes that could be made at the administrative level, but the GSEs’ lending caps could be altered, or the rules for exempting loans from those caps could be changed.