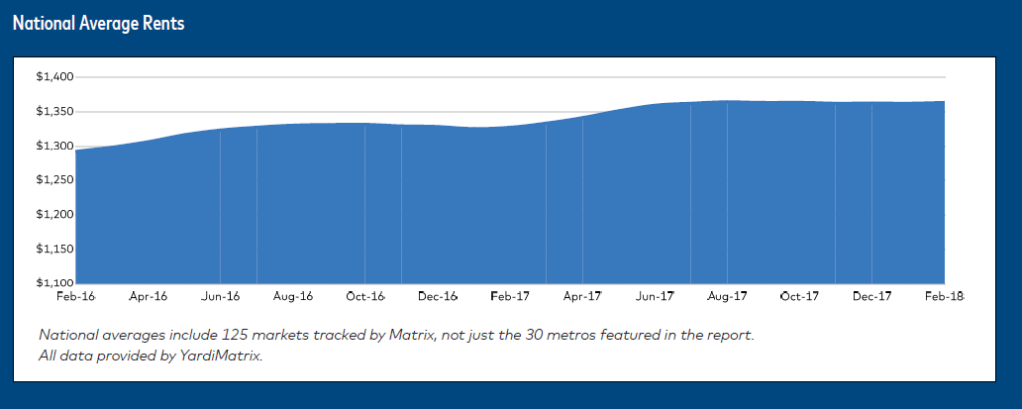

U.S. multifamily rents remained relatively stable in the last month, as average rental rates rose by $1 to $1,364 , according to a new Yardi Matrix report, but rent growth fell to 2.7% year over year (YOY), down 10 basis points from the previous month.

The average U.S. rent has remained within a $2 range between $1,363 and the all-time high of $1,365 since July 2017, and rent growth has fallen very near to the long-term average. This deceleration is not surprising, according to Yardi Matrix, given the long period of above-trend growth in late 2016 and early 2017.

Yardi Matrix expects rent growth to remain moderate in the year to come, given the growing amount of new supply and demand for affordable units in many metros. February 2018’s rent growth marks the weakest gain for any February since the start of the recovery in 2011. Yardi predicts that apartment demand may get a small boost from the effects of the new tax law, as it removes some tax incentives to home ownership, and as such rent growth may pick up soon, as it often does in the first half of the year.

However, some concerns have arisen regarding property fundamentals, inflation, and economic uncertainty. Interest rates are rising, and upcoming tariffs on steel and aluminum – which Yardi Matrix defines as “baffling” – may erode the business confidence that corporate tax cuts and regulatory relief have provided.

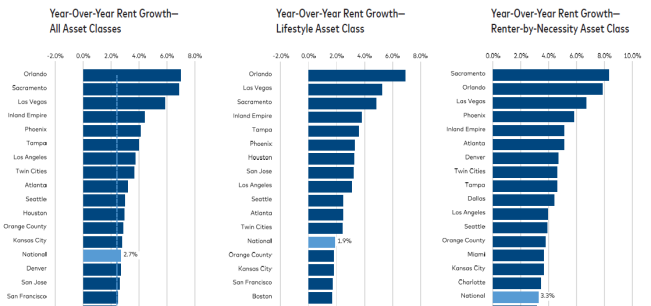

For the first time since June 2016, Sacramento, Calif. is no longer the top metro for YOY rent growth. Orlando took the top spot in February with 7.0% YOY growth, followed by Sacramento at 6.8%. Yardi attributes Orlando’s rise to strong job growth, a steady warm climate, and in-migration resulting from Hurricane Maria.

Rent in Renter-by-Necessity (RBN) properties rose by 3.3%, while rents in Lifestyle properties rose by 1.9%. The gap between workforce and luxury rent growth has grown even wider over the past months, and new luxury property supply remains very high.

On a trailing three-month (T-3) basis, which compares the last three months to the previous three months, rents remained flat nationwide. Orlando led all markets on this basis with 0.6% rent growth, followed by Miami at 0.4%, and Phoenix and the Twin Cities at 0.3%. Yardi notes the Twin Cities are experiencing strong multifamily demand, and have the highest occupancy rate in the country at 97.3%. Austin and Charlotte have the lowest rent growth on this basis at -0.3%.

The metric that tracks most closely with the deceleration in rent growth between 2016 and 2017 is the change in the national occupancy rate, according to Yardi analysis. While occupancy rates are high on a historical basis, they have fallen 60 basis points in each of the last two years.

Yardi connects these drops to the large amount of new supply coming online in many metros. (Metros with strong job growth and strong demand are better able to absorb new units.) Yardi expects that supply growth will hit a peak of 380,000 new units in 2018. As such, rent growth may either level off or continue to decelerate for another year or two.