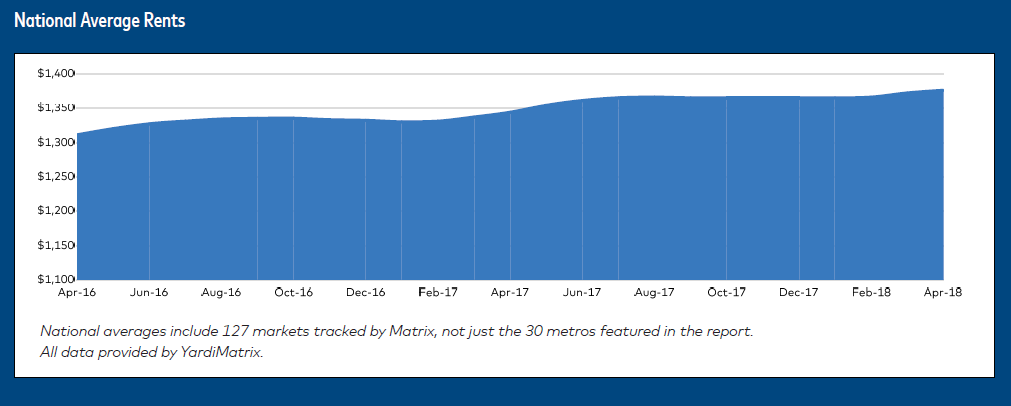

U.S. multifamily rents rose by $4 to $1,381 last month, according to Yardi Matrix’s Matrix Monthly report for May 2018. Multifamily rents have risen by $14 in the last three months and $15 this year to date – a weaker rate of rent growth than the same period last year, when multifamily rents rose $25 from January to May. Rent growth has fallen to 2% year-over-year from 2.5% in April, marking the steepest YOY rent-growth decline in Yardi Matrix’s Matrix Monthly report in more than six years.

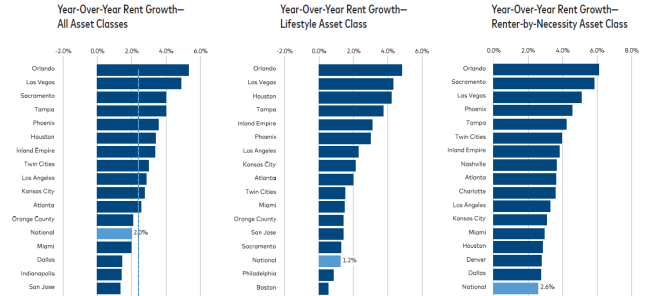

The top four metro markets for rent growth are concentrated in the Southern and Western Sunbelt regions. Only two major metros recorded rent growth above 4.0% YOY this month: Orlando (5.3% YOY) and Las Vegas (4.9% YOY), followed by Sacramento and Tampa at 4.0%. Conversely, a glut of new supply in once-high-growth markets has led to decelerating and even negative rent growth in places such as Austin (-0.5% YOY), Portland (0.4%) and Seattle (0.5%).

On a trailing three-month (T-3) basis, which compares the last three months to the previous three months, rents rose 0.3%. San Jose has posted the highest rent growth on a T-3 basis at 0.7%, followed by Seattle, also at 0.7%. This marks a turnaround for Seattle, as rents declined there at the end of 2017, though high deliveries are expected to keep growth muted.

May’s numbers reflect a two-year pattern of rent deceleration which stems primarily from oversupply in the market. With more than 600,000 new units under construction and expected to be delivered over the next two years, this rent and occupancy pressure is expected to continue, even in high demand markets.

This impact is expected to be especially strong in markets with especially high delivery rates, as well as an oversupply of new luxury apartments which make up 90% of new construction. According to Yardi data, Lifestyle (or luxury) rents are negative on a year-over-year basis in Seattle, Portland, Nashville, Austin and Washington, D.C – all high-growth, high-delivery metros.

Despite these numbers, Yardi reports favorable economic conditions. Job growth is steady, the workforce is near full employment, and overall demand is expected to hold. “But it is important to adjust expectations in the near term,” the report says. “Growth will come—from the right locations and efficient management.”

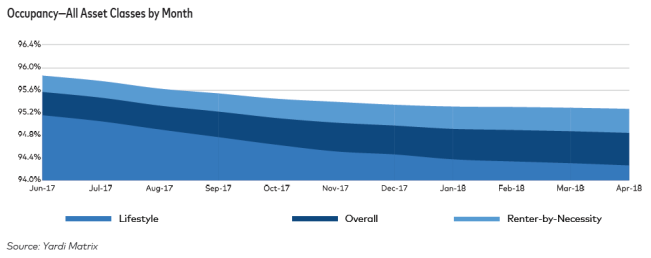

Of Yardi’s top 30 metro markets, only two experienced year over year occupancy increases in April: Phoenix (0.1%) and Houston (0.5%). (Occupancy data is current as of the previous month.) Seattle has experienced the greatest decline at -1.6%, followed by Dallas and Raleigh, N.C. at 1.4%. The national average occupancy rate fell to 94.9% in April 2018, and has fallen 80 basis points year over year.

Yardi notes that while demand is still strong for new units, the sheer supply of new deliveries is likely to continue to soften rent growth and occupancy rates. Over 300,000 new units are expected to be delivered in 2018, most of them luxury units. The disparity in delivery rates for luxury and market-rate units has also created a wide spread between Lifestyle rent growth rates (1.2% YOY) and Renter-by-Necessity rent growth rates (2.6% YOY).

Despite a 17-year low in unemployment and continued, if decelerating job growth, wage inflation remains below 3%. Given this tight labor market, Yardi predicts that wages may rise in the latter half of the year and into 2019, which may increase occupancy rates and mitigate supply issues in affected markets.