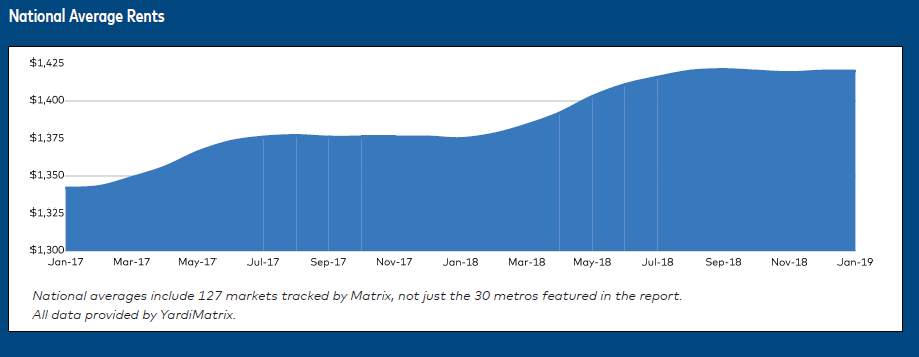

The national average multifamily rent remained at $1,420 in January 2019 while the year-over-year (YOY) rent-growth rate rose 10 basis points (bps), to 3.3%, according to the Matrix Monthly report by Yardi Matrix.

The annual rent-growth rate has remained above 3% for the past six months. While U.S. rents have remained flat since August, Yardi notes that this lack of growth is a normal winter seasonal pattern. Overall, Yardi notes that multifamily continues to run strong, especially compared with other real estate and nonreal estate investment sectors as the cycle continues.

Las Vegas remains the strongest major market for rent growth on a YOY basis, at 7.9%, followed by Phoenix, at 6.5%, and Atlanta, at 5.9%. Each is at or approaching its cycle high for rent growth. Out of the top 30 metros, rents rose by 2% or more in all but three: Houston; Kansas City, Mo.; and Baltimore.

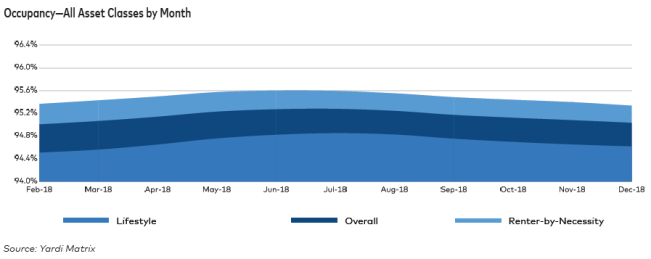

Notably, the gap between “Lifestyle,” luxury rent growth and “Renter-by-Necessity,” workforce rent growth has contracted to 70 bps on a YOY basis, falling under 1% for the first time since 2014.

Rents remained unchanged nationally on a trailing three-month (T-3) basis, which compares the past three months with the previous three months. According to Yardi, this is a good sign for the winter season, when rent growth is historically slow. At the major market level, Las Vegas and Atlanta grew the fastest on a T-3 basis, at 0.2% each. Portland, Ore., ranked lowest, at -0.4%, followed by Indianapolis, at -0.3%.

During the National Multifamily Housing Council’s annual conference in San Diego last month, panelists and speakers were bullish on the sector and by and large expected demand to remain strong across all age sectors. The 20-to-34 age bracket is expected to continue to grow, and some speakers noted that renters above that age are increasingly remaining renters rather than buying homes. According to one speaker, some luxury apartment buildings have found themselves with an average age above 40 and an average income above $200,000.

As the cycle continues, however, return expectations have fallen among both equity and debt investors. Capitalization rates have fallen close to record lows, and interest rates are volatile, according to Yardi. One conference speaker recommended that investors take a look at secondary and tertiary markets, as those assets produce a higher going-in yield.

While Fannie Mae and Freddie Mac have 2019 allocations in place, their future as GSEs remains uncertain, according to Yardi. In addition, high land and regulatory costs continue to make it difficult to build apartment units affordable for middle-class renters. Potential solutions include modular construction, subsidies, and consistent enforcement of existing rules.