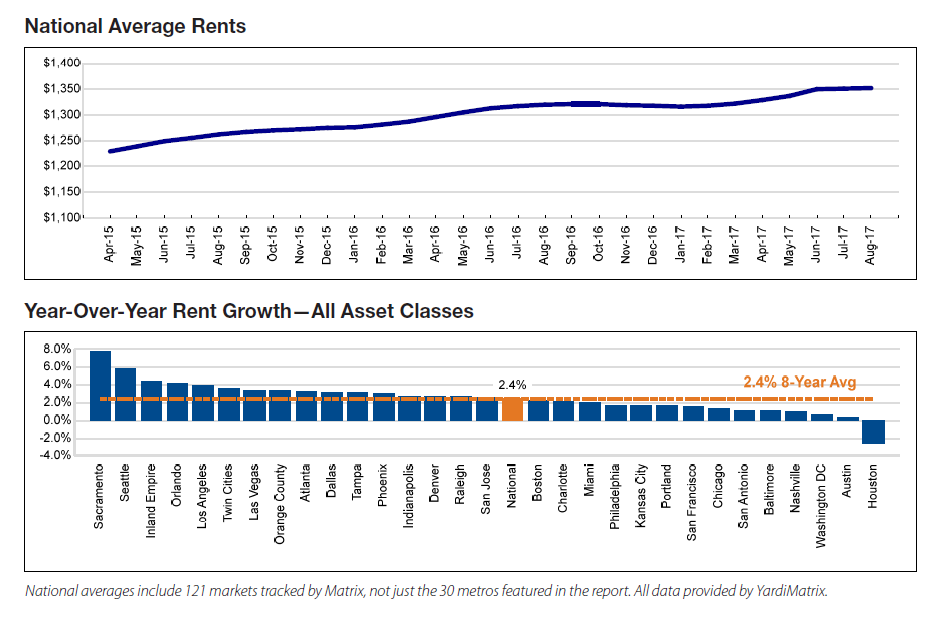

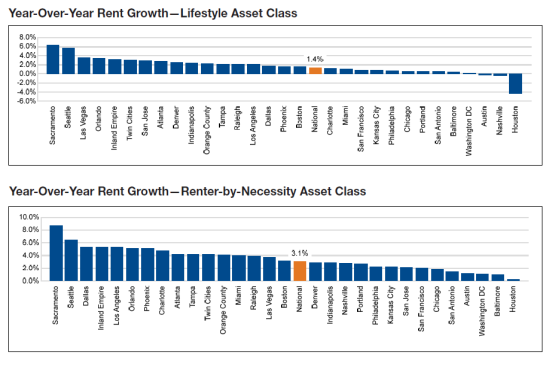

The average U.S. monthly rent rose by $1, to $1,352, in August, remaining essentially flat as apartment completions begin to slow across many of the 121 markets in Yardi Matrix’s Matrix Monthly survey. Meanwhile, the national rent-growth rate fell to 2.4%, down 20 basis points (bps) from July. (Despite these slowdowns, rents have increased every month this year.) Economic conditions and multifamily demand remain strong.

New-apartment deliveries averaged 17,700 per month in 2016 but fell to 14,500 per month in the first quarter of 2017, 12,700 in the second quarter, and less than 10,000 in July and August. The slowing new luxury-unit supply could mark a turning point for decelerating rent-growth trends in oversupplied markets, notes Yardi. Examples include Austin, Texas, where rent growth had fallen to 0.3% year over year (YOY) as of August, and San Francisco, which fell from double-digit YOY rent growth to 1.6% YOY growth last month.

Yardi Matrix’s database shows that about one-third of the 480,000 new apartment units are being delayed by an average of 7.5 months. Yardi attributes the delays to a critical shortage of construction workers, now exacerbated by the Trump administration’s restrictive immigration policies. As a result, Yardi is reducing its new-delivery forecast to 300,000 new units in 2017, down from its previous forecast of 360,000. The company now predicts that supply will peak at 360,000 in 2018.

Overall, occupancy of stabilized properties remained unchanged from June 2017, at 95.6%, to July 2017, when it was down 20 bps YOY. (Yardi Matrix’s occupancy data are current as of the month prior to that for the rent and rent-growth data.) The occupancy for market-rate, or “Renter by Necessity” (RBN), properties is 95.8%, while the occupancy rate for luxury, “Lifestyle,” properties is 95.3%—a 50 bps spread between the two types of assets. Yardi notes that the spread has narrowed over the course of this year as new luxury units have been absorbed.

On a trailing three-month (T-3) basis, rents rose by 0.4% nationwide in August, down 10 bps from July. Lifestyle rent growth outperformed RBN rent growth on this basis, 0.4% to 0.3%.

As noted above, rents have stabilized in some markets as new supply is absorbed and incoming supply is delayed. These include Seattle, which experienced 0.8% rent growth on a T-3 basis in August, as well as Denver (0.6%), Boston (0.6%), and San Francisco and San Jose, Calif. (both at 0.5%).

On a trailing 12-month basis (T-12), rents grew 3.1% YOY last month, down 10 bps from July. RBN rent growth (4.1%) outpaced Lifestyle rent growth (1.9%) on this scale. Lifestyle rent growth has fallen below 2% on a T-12 basis for the first time since 2011. Sacramento, Calif., remains the strongest market, at 9.6% growth on a T-12 basis.

Houston remains the only market experiencing declining rent growth on a T-3 or T-12 basis, with -0.1% growth on a T-3 basis and nearly -2.0% growth on a T-12 basis. While Yardi notes that it is far too early to assess the impact that Hurricane Harvey’s damage will have on Houston’s apartment market and rent trends in the coming months, the firm predicts that multifamily fundamentals could benefit as damaged stock is taken off the market and residents turn to rentals for temporary or permanent housing.