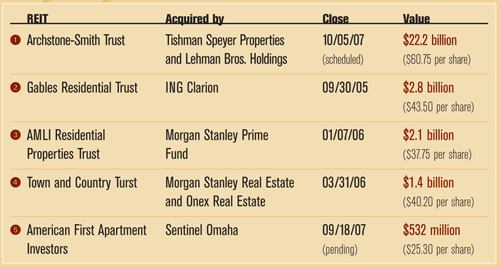

Still, without shareholders and analysts to answer to, private equity firms generally find it easier to stomach the task of flipping properties. That way, they can cash out equity for pocket and pipeline alike. Case in point: Gables sold off 27 percent of its properties in its first post-acquisition year, according to MFE’s 2007 Top 50 data. The firm also has plans to expand its development pipeline throughout 2007 and beyond.

THIS IS NOW Today, the deals seem to be more financially motivated than strategic power plays. A closer look at the pending Archstone merger provides some insight, but also demonstrates that there is never a sure bet in this industry.

For instance, some observers expect an even more aggressive sell down of assets, if not an all-out fire sale, as the Archstone deal inches closer. “If they are able to [close] that transaction, there will be a significant sell-off of assets,” Fryer predicts. Indeed, the expectation that Archstone is more of a financial play—that Tishman Speyer and Lehman Bros. will essentially flip the portfolio in several smaller asset sales—would partially explain the merger delay.

“These deals are so much more than a real estate play—it’s buy a deal at wholesale and make the spread between five or six retail sales,” says McManus, who expects that—similar to the sale and resale of Equity Office Properties following its privatization by the Blackstone Group—the buyers of the Archstone properties will make flips of their own.

Yet, in its merger proxy statement filed with the SEC, Archstone details several meetings with Tishman Speyer and Lehman Bros. representatives where the JV expressed a keen interest in growing—as opposed to liquidating—the company’s multifamily portfolio. In particular, on three separate occasions between May 14 and May 20, the JV stipulated that retention of the senior management team was a crucial component of its acquisition offer and strategic plans for building off the company’s platform. That hardly seems the comments of a firm contemplating a piecemeal divestiture of its purchase.

Beth DiSanto, founding partner of the Corporate and Real Estate Law Group at DiSanto and Associates and a speaker at this month’s Global REIT Symposium, is one to take the JV’s stated intentions at face value. “I think the most prominent trend right now is for the larger companies to try to dominate a sector, and I expect that is going to continue,” she says. “It makes sense for them to use their economies of scale to develop huge portfolios … and become the biggest player in the market.”

WHO’S NEXT One thing’s for certain. Until the Archstone deal either concludes or collapses, the jury is out on what to expect in terms of future multifamily REIT privatizations. While elementary economics suggest that firms will continue to both enter and exit the public arena, MFE’s industry panel declined to guess the next REIT to privatize. Part of the diffidence lies understandably in confidentiality agreements that these industry vets must honor with their clients, but that very activity indicates that, clearly, something is going on.

“In terms of scale transactions, I would be surprised if something happened [before] the debt market settles; there is more certainty around execution risk,” says Fryer, who thinks future REIT privatizations likely will return to smaller strategic plays. Acquirers will seek specific developments or executive talent or look to grow market share in a particular region.

And even though everyone seems to be holding their breath until the effects of the subprime crash ebb away, pundits say that in real estate, there’s always the possibility that someone makes their move when market distractions have everyone else’s attention. “I think there are a lot of private equity funds and companies that are well positioned to complete these mergers without having to get any credit, especially on the smaller side,” DiSanto says. “I don’t think the credit crunch will stop these deals—it might slow them down, but I do not see it as a major deterrent.”

Menna agrees, and he says he wouldn’t be surprised to suddenly hear of an unsolicited—though not yet public—bid on a multifamily apartment REIT, large or small. “I’m here to tell you for certain that there are people looking at privatizing multifamily companies and they are looking at doing it in today’s environment,” he says. “There are cash-rich buyers out there … that have large cash reserves that might—just might—come to the conclusion that there is a buying opportunity based on today’s valuations.”