Meet the Panel

Beth DiSanto

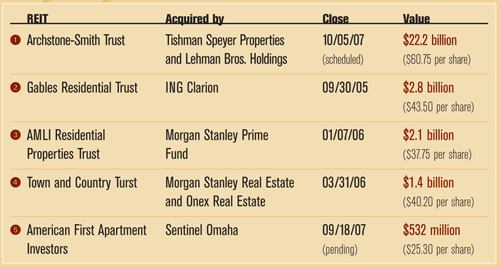

Q: What is the likelihood of the Archstone-Smith privatization occurring?

A: From the legal side, I suspect that there were a lot of things that were not contemplated in the Archstone deal, so I expect that there will be some bumps in the road. But I think it is going to happen. They can delay all they want, but that train has already left the station.

A REIT specialist involved in several multifamily IPOs, Beth DiSanto is founding partner of the DiSanto and Associates law firm where she heads up the Corporate and Real Estate Law Group.

Bill Fryer

Q: What multifamily REIT privatization trends do you expect over the next year?

A: We are just at that period where we have had a significant level of activity and we well settle out now. But I don’t see any train wrecks—I don’t know of anyone who has done a transaction over the last several years and is unhappy about having done it.

Bill Fryer is the senior partner and head of the Real Estate Market Capital Practice Group in the New York, Atlanta, and London offices of Atlanta-based law firm King and Spalding. He also acted as a buyer’s advisor during the privatization of both Gables Residential Trust and AMLI residential trust.

Richard Gollis

Q: What types of REITs do you think offer a good buyers’ premium?

A: We look at the ones with the best market insulation relative to current trends in the real estate industry. [These are] companies that are focused in urban areas with high job growth and high barriers to entry—much like an Archstone-Smith and AvalonBay. Those kinds of companies are the ones that most likely will fare best in current environments.

Richard Gollis is a principal for The Concord Group, a real estate investment advisory firm based in San Francisco that specializes in providing multifamily market intelligence to top private equity investment firms.

Matt McManus

Q: What makes privatization both attractive and risky to private equity?

A: They can swoop in, buy an entire portfolio and have an immediate locked-in premium just by the difference between the stock price and the conservative estimate value of the real estate. So the privatizations today are really financing gambles. Are they supported by underlying real estate fundamentals? Yes, but the spreads are being dictated by how much the next buyer can pay.

Matt McManus is the chairman of Bluestone Real Estate Capital, a Philadelphia-based commercial real estate investment bank and private equity investor that sources and arranges financing. The firm also acts as a financial advisor for public and private companies.

Gill Menna

Q: What is the likelihood of an Archstone-type deal being announced in today’s real estate climate?

A: No one is doing any CMBS, no one is underwriting any securitized product. The expectation with what has happened here is that with the sub-prime losses, the entire structured financing market is going to fall down. I think that will all eventually get rationalized, but for now, you just can’t get debt done. So [such a] deal would be next to impossible.

A partner at Boston-based law firm Goodwin and Proctor, Gill Menna chairs the firm’s REITs & Real Estate Capital Markets Group. He was involved in the sale of Gables Residential to ING Clarion and Lehman Bros. as well as the sale of Summit Properties to Camden Properties Trust.

Michael Stewart

Q: What REITs do you think are up next to be privatized?

A: AIMCO and Equity Residential are big players and seem like they would be pretty attractive deals. Obviously, I have not seen every property in their portfolio, but they are clearly well positioned in a lot of markets. I’ve seen several dozen of their properties in Phoenix and I wouldn’t mind having them—if I could get them for the right price.

Michael Stewart is the president of Pacific Property Assets, an Irvine, Calif.-based private multifamily apartment owner of approximately 5,800 units, that competes with REITs across the Southern California and Arizona markets.